策略实现#

示例策略#

通常情况下,策略会有多个指标,且之间有较复杂的依赖关系,此时TradePy会通过指标函数的参数声明,推断出正确的指标计算顺序。因而,使用TradePy时,您只需关注指每个标计如何计算和以及判断买卖信号。

提示

该示例代码可在 快速上手 教程中找到。

单函数,多指标#

如果您的策略有很多计算方式雷同的指标(比如均线),那么每个均线指标单独写一个计算方法,或许显得有些冗余。TradePy提供了一种更简洁的写法,可以用单个函数计算多个指标。借此可以简化上述的实现:

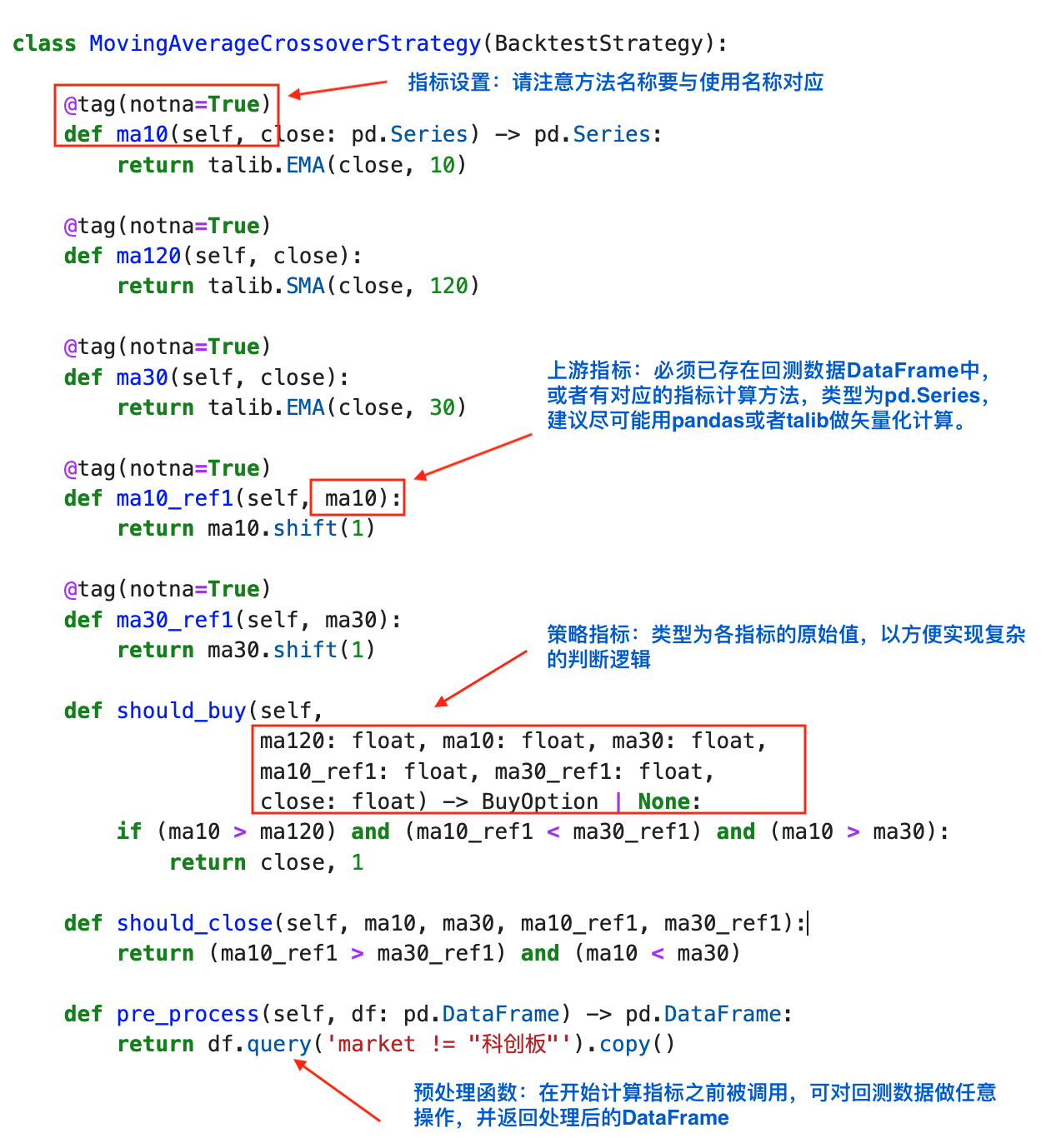

class MovingAverageCrossoverStrategy(BacktestStrategy):

# outputs: 输出指标的名称

@tag(outputs=["ma10", "ma30", "ma120"], notna=True)

def moving_averages(self, close):

# 逐个返回指标结果,注意顺序要和outputs对应

return talib.EMA(close, 10), talib.SMA(close, 30), talib.SMA(close, 120)

@tag(outputs=["ma10_ref1", "ma30_ref1"], notna=True)

def moving_averages_ref1(self, ma10, ma30) -> pd.Series:

return ma10.shift(1), ma30.shift(1)

def should_buy(self, sma120, ema10, sma30,

ema10_ref1, sma30_ref1, close, company) -> BuyOption | None:

if "ST" not in company:

if (ema10 > sma120) and (ema10_ref1 < sma30_ref1) and (ema10 > sma30):

return close, 1

def should_sell(self, ema10, sma30, ema10_ref1, sma30_ref1):

return (ema10_ref1 > sma30_ref1) and (ema10 < sma30)

def pre_process(self, df: pd.DataFrame) -> pd.DataFrame:

return df.query('market != "科创板"').copy()

内置指标#

5均、10均、20均、MACD之类的常用指标,也没有必要每个策略中都重复实现一遍。让策略类继承 FactorsMixin,则可直接开始使用各类常用指标,具体可用指标请查阅 FactorsMixin 的实现。

现在,我们可以进一步简化策略的实现,只留下”前一日指标”部分的计算方法:

from tradepy.strategy.factors import FactorsMixin

class MovingAverageCrossoverStrategy(BacktestStrategy, FactorsMixin):

@tag(outputs=["ema10_ref1", "sma30_ref1"], notna=True)

def moving_averages_ref1(self, ema10, sma30) -> pd.Series:

return ema10.shift(1), sma30.shift(1)

def should_buy(self, sma120, ema10, sma30,

ema10_ref1, sma30_ref1, close, company) -> BuyOption | None:

if "ST" not in company:

if (ema10 > sma120) and (ema10_ref1 < sma30_ref1) and (ema10 > sma30):

return close, 1

def should_sell(self, ema10, sma30, ema10_ref1, sma30_ref1):

return (ema10_ref1 > sma30_ref1) and (ema10 < sma30)

def pre_process(self, df: pd.DataFrame) -> pd.DataFrame:

return df.query('market != "科创板"').copy()

可调参数#

在开发策略时,一般无法最初就确定最佳的参数组合(比如均线类型、RSI周期、布林带周期、止损止盈点位),而需要反复回测以找到预期收益最大的一组参数。

TradePy支持通过 StrategyConf.custom_params 提供自定义参数,即可在策略类中直接在 self 上访问参数值。继续用同样的例子,我们可以再加一个策略逻辑“只买入股价在某个最低值以上的股票”:

提示

请参考”寻参优化”教程

from tradepy.strategy.factors import FactorsMixin

from tradepy.core.conf import BacktestConf, StrategyConf

class MovingAverageCrossoverStrategy(BacktestStrategy, FactorsMixin):

# 其他不变 ...

def should_buy(self, sma120, ema10, sma30, orig_open,

ema10_ref1, sma30_ref1, close, company) -> BuyOption | None:

if "ST" not in company:

# `orig_open`由TradePy提供,是未复权前的实际开盘价

if orig_open >= self.min_stock_price:

if (ema10 > sma120) and (ema10_ref1 < sma30_ref1) and (ema10 > sma30):

return close, 1

conf = BacktestConf(

cash_amount=1e5,

strategy=StrategyConf(

stop_loss=4.5,

take_profit=3,

custom_params={

# 自定义参数在这里

"min_stock_price": 5

}

)

)

MovingAverageCrossoverStrategy.backtest(df, conf)

API#

- class tradepy.strategy.factors.FactorsMixin#

- atr(high, low, close)#

平均真实价格波动

atr_period: 均值周期,默认14

- boll(close)#

布林带, 自定义参数:

boll_period: 均值周期, 默认20

boll_dev_up: 上轨标准差, 默认2

boll_dev_down: 下轨标准差, 默认2

输出指标: boll_lower, boll_middle, boll_upper

- ema10(close: Series)#

指数移动10均

- ema120(close: Series)#

指数移动120均

- ema20(close: Series)#

指数移动20均

- ema250(close: Series)#

指数移动250均

- ema30(close: Series)#

指数移动30均

- ema5(close: Series)#

指数移动5均

- ema60(close: Series)#

指数移动60均

- macd(close: Series)#

MACD指标

- rsi(close)#

RSI, 自定义参数:

rsi_fast_period: 快周期, 默认6

rsi_mid_period: 中周期, 默认12

rsi_slow_period: 慢周期, 默认24

输出指标: rsi_fast, rsi_mid, rsi_slow

- skdj(close: Series, low: Series, high: Series)#

SKDJ - 慢速随机指标

输出指标: sdj_k, sdj_d

- sma10(close: Series)#

简单移动10均

- sma120(close: Series)#

简单移动120均

- sma20(close: Series)#

简单移动20均

- sma250(close: Series)#

简单移动250均

- sma30(close: Series)#

简单移动30均

- sma5(close: Series)#

简单移动5均

- sma60(close: Series)#

简单移动60均

- typical_price(high, low, close)#

典型价格 = (high + low + close) / 3